2023 review - edit

- Ben Fillmore

- Dec 13, 2023

- 6 min read

Updated: Feb 2, 2024

So updating this post to close out 2023 properly, with final year numbers..

It's been an interesting year, starting well, having a very flat and boring spring, and then finishing strong.

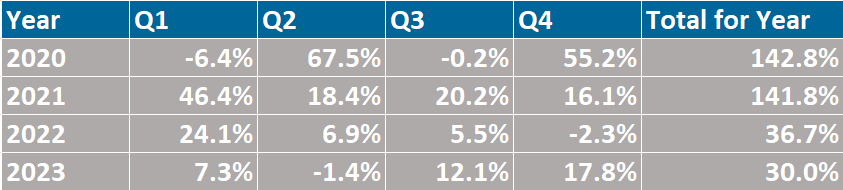

Our consolidated portfolio performance finished up 30.0% which is a slight beat on the S&P 500 which came in at 24% up. However, the S&P 500 is only up following the strong performance of its 7 largest entries, all of which could easily be argued are overvalued on pretty much any metric and represent significant downside risk.

If we take away the big seven, then the "S&P 493" had a much smaller gain of 6% during 2023. Given the purpose of our portfolio is to protect against declines whilst providing asymmetrical upside potential, we feel that a return of ~30% versus an essentially flat, but in our view riskier, market is a good return and continues the strong performance we have produced since 1 January 2020.

The "S&P 493" this year versus the full index

Our portfolio now has achieved a cumulative return of 936% since 1 Jan 2020, or an annualised return of 79% across a period of 4 years. The smaller returns in 2022 of 36% and 2023 of 30% reflect a reduction in risk appetite during this period compared to 2020 and 2021, although have still produced outsized returns, so overall I am happy with the progress and "maturing" of the portfolio.

This year has been one of searching for new themes, whilst old ones mature.

Uranium We have remained invested in uranium, though we exited most general equities during late 2021 - early 2022, but kept a position in physical via both U.UN and YCA.L. During late 2022 and early 2023 we recommenced some positions in juniors wherever we saw value. Some of those have now been partially exited in the recent run-up. But we have generally been moving profits from equities to increasing our position in physical, letting that run. Our feeling is that there is further upside to come in physical, however equities need to see a sustained spot price to maintain their current levels, outside of a few exploration stories. We think we may see spot uranium prices peaking mid-late 2024, and we are expecting some detachment from the physical vehicles to spot. We believe this has started showing already with YCA.L maintaining a greater than 10% discount in this run and U.UN often having a 5-10% discount. Any spike in spot may see those discounts widening. We have our exit strategy that was laid out in 2019 which we are sticking to. We are happy if that means we leave some money on the table for someone else, our returns more than compensate for not calling the precise top.

UK Housebuilders A new theme for us that opened up during 2022 is UK housebuilders. Equities were down >50% from their 2021 peaks and despite a rising rate environment, we felt that the market had overly compensated. Some of these have large land banks that in a tight development market like the UK are not easily reproducible. It had gotten to the point where the equities were trading for less than their land value, which even in a 'higher for longer' rate climate, seemed overly punitive. Having commenced positions in late 2022 and continuing to add on weakness during 2023 this theme has become a ~15% portfolio position for us, spread across key equities. With a return thus far of c15% we feel we are through the worst and there is plenty of upside remaining. We will add a final tranche on any future dip taking our portfolio exposure to 20%, if the market allows.

Other value plays

We have been building positions in a few various value plays during late 2022 and into 2023. We have increased exposure to BATS.L and IMB.L with the belief both companies are currently priced like they only have a few years of profitable trading left, and we have continued to add to both through 2023. We see both beating expectations over time and expect this position to reward us over a period of 5 years.

We also like the central and eastern Europe fund, CEE, which is a sleeping giant in our opinion. They hold a large amount of locally converted ADRs in various Russian equities, that are currently on their books at 0 value. We don't believe the current sanctions will hold indefinitely, and we are confident some mutual trading of positions will be allowed in the not-so-distant future. If you apply their book value (i.e. full Moscow value) then CEE would have a NAV of >$20 per share, i.e. more than double. Even applying a 50% discount to the Russian assets, after Putin has taken his slice, it has a NAV of $15, i.e. a 50% return. We believe we'll see an agreement to swap assets prior to end of 2024, so that's a healthy annualised return. The downside - the fund otherwise is mostly invested in reasonable dividend paying companies based in value countries like Poland and Hungary, so even forgetting the Russian assets, it's still interesting, and with limited downside risks.

Other commodities

We have been increasing exposure tentatively into other sectors in the commodities space as prices come back to Earth. We like gold miners here, with the metal near/at all time highs yet with miners down 50-90% from their recent peaks. Whilst things were bubbly three years ago, the market has been brutal for many decent companies that are now available on sale. We are still building positions but at present there are many that are offering value for money.

Shorts We believe remaining hedged in an environment where there are plenty of large assets are historically high valuations is wise. At present our hedges are primarily against NVDA - with a variety of LEAPS out into 2025 and beyond at strike prices of between 225 and 325. Time will tell whether they'll pay off, but we sleep better knowing we have some downside protection.

Pair trades With returns harder to find, we have had to work a little harder this year to generate alpha. We have enjoyed two successful pair trades which have now both been exited. Firstly we noticed a disconnect between WHC and NHC. We went long WHC and short NHC. News flow helped close the gap faster than we had imagined. Another was the disparity between BDRY and a basket of dry bulk shipping companies. The equities had held up much better than should have been the case given the collapse in capesize rates. Long BDRY and short the equities. Well capesizes nearly doubled in the space of a few weeks in Nov/early Dec and provided a short term exit from this pair trade, with a yield over 100% in a few months. We believe should capesize rates normalise in early Jan/Feb there is a chance to re-establish this trade.

WHC vs NHC over two years, nice gap opened up that was promptly closed.

Basket of dry bulk co's vs BDRY index - disconnect to reduce

Looking into 2024, what's on our radar?

We expect to see a continuation of rising uranium prices, perhaps culminating in a peak next year. Let's not forget that ultimately this market is balanced at $85/lb uranium, and spot is there as of writing. With limited new production hitting the market pre 2027/2028 we see pricing having to go to the margins. What is a utility prepared to pay to secure supply? We believe this is why equities have stalled and spot continued to run, as most serious money knows the market is in equilibrium at $80 U which is already priced into the equities. With contracting taking place a few years out, next year or 2025 should mark the peak in marginal pricing. With supportive U prices, a lot of production will come on which will no doubt soften prices further out on the curve. So if we're going to see a spike, in our opinion this is likely in 2024/5.

We are watching closely the commercial real estate market, and whilst perhaps the best bargains are behind us, we think this sector is going to take longer to turn around than many are pricing in currently, and we may see a dip again during 2024 as shorter-term investors rotate out.

Whatever else we look at, we are staying away from growth and remain focused on value.

Here's to a good 2023 and looking forward to whatever 2024 may bring,

Ben Fillmore

Comments